Can I bring a Claim for Personal Injury Sustained in a Car Accident?

Car accidents in Ontario don’t end at the scene. The physical injuries, the confusion about insurance, the question of whether you can even sue - it’s a lot to sort through under a system most people misunderstand. Ontario runs a threshold no-fault insurance model, which means some claims go through your own insurer and others go to court, depending on the severity of what happened. This article breaks down how both paths work, what the threshold actually requires, and where direct compensation fits in. Bruce Cook at Cook Reynolds in Hamilton has handled these cases across the province’s personal injury spectrum for years.

Last updated on 4/15/2026

What to Do After a Car Accident in Ontario

The first few hours and days after a car accident matter more than most people realize. What you do at the scene and in the weeks that follow can shape your legal options down the road.

If you’re able to, stay at the scene and call 911 when there are injuries or significant vehicle damage. Exchange insurance and contact information with the other driver. Take photos of the vehicles, the road conditions, any visible injuries, and anything else that might be relevant later. If there are witnesses, get their names and numbers.

See a doctor as soon as possible, whether or not you feel fine. Soft tissue injuries, concussions, and spinal problems often don’t show symptoms right away. A medical record from the day of the accident or the day after creates a paper trail that connects your injuries to the collision. Without it, insurers and defence lawyers will argue the injuries came from somewhere else.

Report the accident to your own insurance company promptly. Under Ontario’s accident benefits system, you have 30 days to submit your application if you want to apply for statutory accident benefits. Missing that window can create problems.

Why People Think They Can’t Sue After a Car Accident

A lot of people assume they’ve lost the right to sue after a car accident in Ontario. That’s not quite right.

The confusion traces back to 1990 when the provincial government passed the Ontario Motorist Protection Plan. The media called it a "no-fault system," and the label stuck. But Ontario’s system isn’t pure no-fault. It’s a hybrid - what’s formally known as a "threshold no-fault" system. Below a certain severity threshold, you can’t sue. Above it, you can.

The 1990 legislation modelled itself on Michigan’s system. The idea was straightforward: keep minor or temporary injuries out of the courts, reduce claims costs for insurers, and hold premiums down. Only the most serious cases would go before a judge.

In exchange for restricting the right to sue, the government built enhanced accident benefits into every auto insurance policy. Those benefits - income replacement, medical and rehabilitation coverage, attendant care - became known as "no-fault benefits." That phrase added another layer of confusion, and here we are thirty-five years later still untangling it.

Direct Compensation for Property Damage

There’s a second piece of legislation that trips people up. Ontario has a direct compensation regime for property damage. You used to be able to sue the at-fault driver for damage to your vehicle. Now, property damage claims go through your own insurer. The two insurance companies sort out reimbursement behind the scenes.

That process reinforces the "you can’t sue anyone" misperception. But it only applies to property damage. The right to sue for personal injuries is a separate question entirely.

Accident Benefits and Tort Claims: Two Separate Tracks

If you’ve been hurt in a car accident in Ontario, there are two separate avenues for seeking compensation, and they run on different tracks with different rules.

The first is an accident benefits claim against your own insurer under the Statutory Accident Benefits Schedule. These are the "no-fault" benefits built into your auto policy. They can include income replacement (up to a percentage of your gross income), medical and rehabilitation coverage, attendant care for people who need help with daily tasks, and non-earner benefits for those who weren’t working at the time of the accident. You file this claim with your own insurer regardless of who caused the crash.

The second is a tort claim - a lawsuit against the person who caused the accident. This is where you pursue compensation for pain and suffering (general damages), past and future income loss beyond what accident benefits cover, and the cost of care that isn’t covered by your policy. The tort claim is the one that faces the threshold test.

You can pursue both at the same time. They’re not either-or. But the processes, deadlines, and rules are different for each, and what you receive through accident benefits can affect what you recover in a tort claim. Most people find they need help sorting through the overlap.

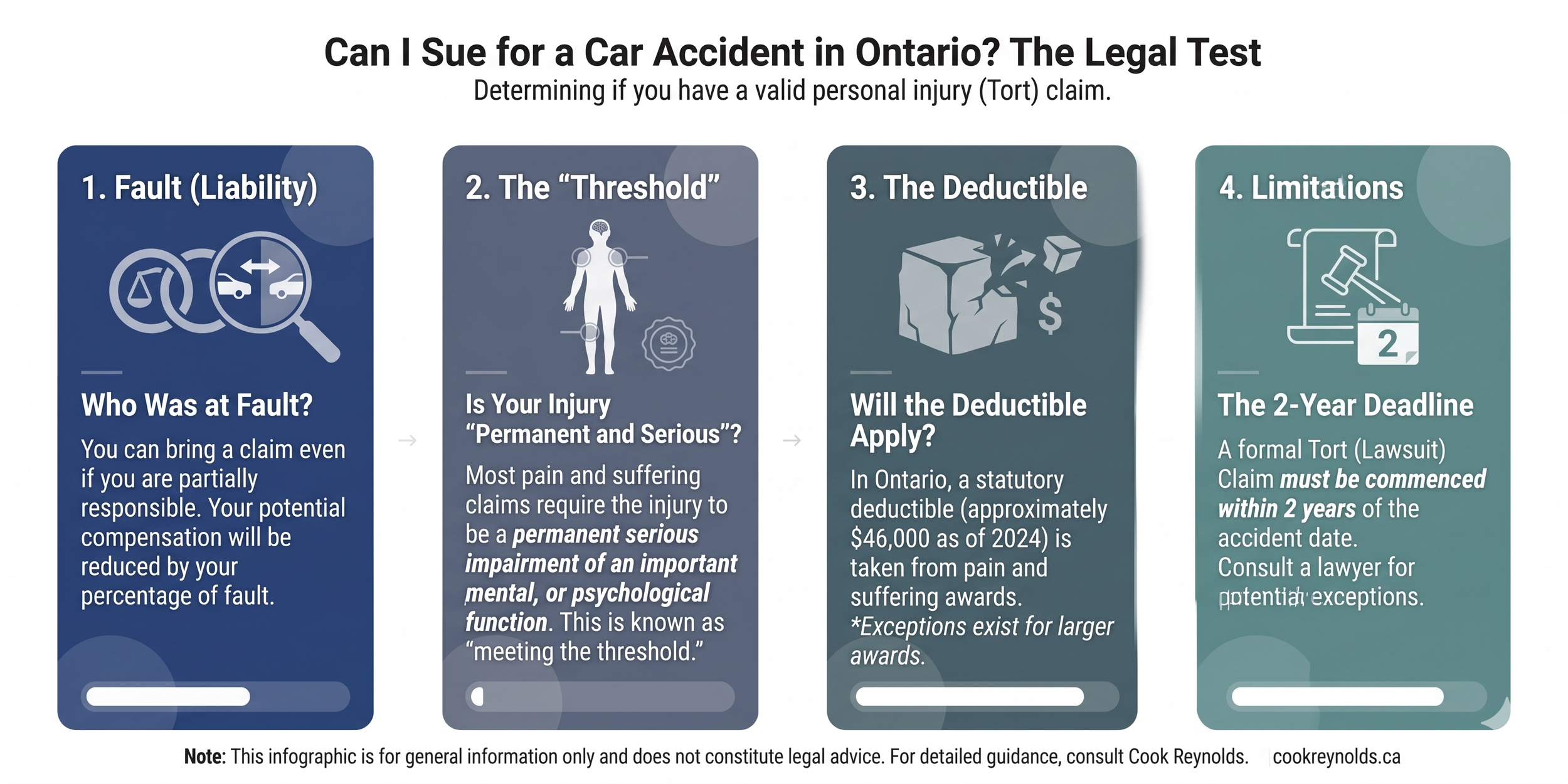

The Threshold: What You Need to Prove

The tort side has a gate. Under section 267.5 of the Insurance Act, you need to show a serious and permanent impairment of an important physical, mental, or psychological function to claim general damages or care costs in court.

"Serious" means the impairment interferes with your ability to do your regular job, continue training for a career, or carry out most of your daily activities given your age. "Permanent" means continuous since the accident and not expected to substantially improve even with reasonable participation in recommended treatment.

In practice, the threshold catches injuries like chronic pain conditions that don’t resolve, traumatic brain injuries, spinal damage with lasting limitations, and psychological conditions like PTSD that persist long after the accident. The defence will almost always argue the threshold hasn’t been met, which is one of the most contested areas in motor vehicle accident litigation in Ontario.

That’s the threshold for general damages and care costs. It doesn’t apply to everything.

You don’t need to meet the threshold to claim a loss of income or loss of competitive advantage. And the threshold restrictions only apply to certain defendants known as "protected defendants" - typically insured drivers. There can be parties in a car accident case where the threshold doesn’t apply at all.

Ontario’s Statutory Deductible

Even when you clear the threshold, there’s another wrinkle most people don’t know about. Ontario applies a statutory deductible to non-catastrophic general damage awards. If a judge or jury awards you compensation for pain and suffering, the province automatically reduces that award by a fixed dollar amount set by regulation.

The deductible is indexed and adjusted periodically. It only disappears once your general damages award exceeds a second, higher dollar amount. Below that ceiling, every award gets reduced. For someone with a moderate-to-serious injury that doesn’t meet the catastrophic impairment definition, this deductible can take a meaningful chunk out of the final number.

This is one of the reasons settlement negotiations in Ontario car accident cases look different from what people expect. A lawyer who concentrates in this area will factor the deductible into case valuation from the start, not as an afterthought.

How Long You Have to Sue After a Car Accident

Ontario’s Limitations Act, 2002 sets a two-year limitation period for most personal injury claims. The clock starts on the day you knew or should have known you had a claim - not necessarily the date of the accident. That distinction matters for injuries that surface weeks or months later.

For minors, the limitation period doesn’t start running until they turn eighteen. And there are other exceptions for people under disability or situations involving government entities where shorter notice periods apply.

The accident benefits side has its own deadlines. You have 30 days to notify your insurer after the accident, and specific windows to submit applications for different categories of benefits. Missing a limitation period or a notice deadline can permanently close the door on a claim, so these dates deserve attention early.

Getting the System Right Has Been Difficult

Since 1990, Ontario has made roughly five major overhauls to this system and dozens of smaller amendments. The balance between restricting court access and protecting injured people keeps shifting. Having a lawyer who concentrates in personal injury law matters here - they can tell you which version of the rules applies to your accident date, what you can claim in tort, and what falls under accident benefits.

This post is for information purposes only and isn’t legal advice. If you’ve been injured in a car accident in Hamilton, Burlington, Niagara Falls, Brampton, Mississauga, or another city in Southern Ontario,contact Cook Reynolds or another lawyer experienced in personal injury law to find out where you stand.

Frequently Asked Questions

Can I Sue for Pain and Suffering After a Car Accident in Ontario?

You can, but only if your injuries meet the threshold test under section 267.5 of the Insurance Act. You need a serious and permanent impairment of an important physical, mental, or psychological function. Temporary injuries or ones that resolve with treatment won’t clear the bar. If your injuries do meet the threshold, you can pursue a tort claim for general damages (pain and suffering) against the at-fault driver.

How Much Is a Car Accident Settlement in Ontario?

There’s no standard number. Settlement amounts depend on the severity of your injuries, the strength of the medical evidence, how much income you’ve lost, what your future care needs look like, and whether the threshold and statutory deductible apply. Cases range from five figures for moderate injuries to seven figures for catastrophic ones. A personal injury lawyer can give you a realistic range once they’ve reviewed your medical records and the facts of the accident.

Do I Need a Lawyer for an Accident Benefits Claim?

Strictly speaking, no - you can file an accident benefits claim on your own. But the process is complex. Insurers regularly deny or reduce benefits, and disputes over treatment plans, income replacement amounts, and catastrophic impairment designations are common. Many people start the process themselves and bring in a lawyer experienced in insurance disputes once they hit resistance. The earlier you get advice, the fewer mistakes there are to fix later.